3Q Multifamily Developer Sentiment Was Mixed

Confidence in the market for new multifamily homes was mixed year on year in the third quarter of 2024, according to the National Association of Home Builders’ (NAHB) Multifamily Market Survey (MMS).

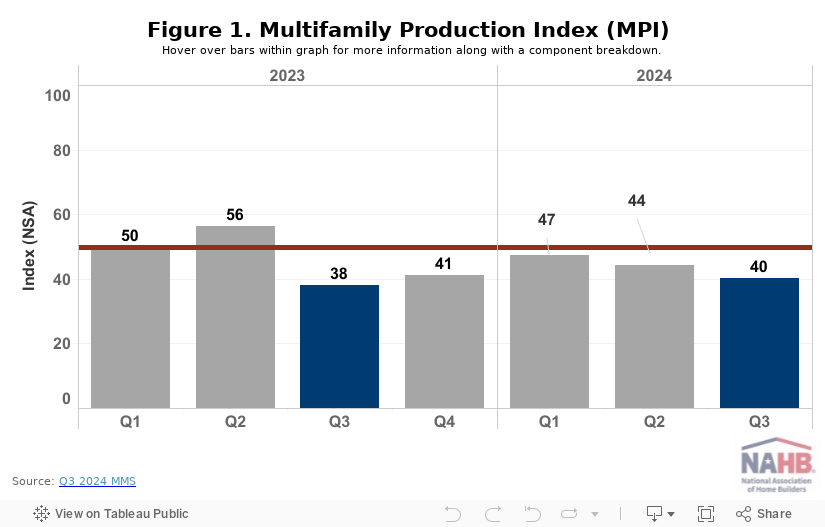

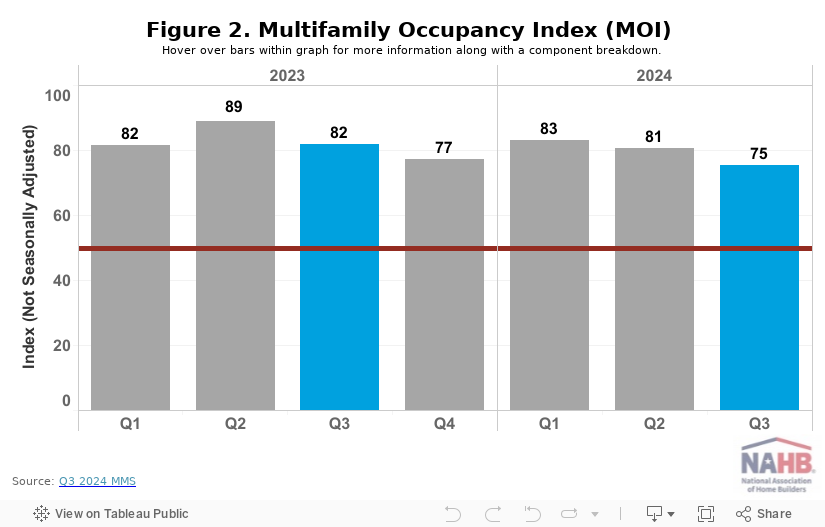

The MMS generates two distinct indices: the Multifamily Production Index (MPI) was 40, up two points year on year, and the Multifamily Occupancy Index (MOI) was 75, down seven points year on year.

While demand for rental apartments remains strong enough to support relatively high occupancy rates in existing projects, multifamily builders and developers continue to face numerous significant barriers to new projects, including higher construction costs, the cost and availability of financing, and land and regulations.

NAHB expects multifamily development to continue poor for another year as the market works through a large number of units under construction, before returning to long-term patterns near the end of 2025.

Multifamily Production Index (MPI)

The MPI is a weighted average of four important market segments: three built-for-rent (garden/low-rise, mid/high-rise, and subsidized) and one built-for-sale (or condominium).

The poll asks multifamily builders to rank current circumstances as “good,” “fair,” or “poor” for multifamily starts in markets where they operate.

The measure and its components are scaled so that a score greater than 50 indicates that more respondents rate conditions as favorable rather than poor.

Two of the four components had year-over-year increases: the component assessing subsidized units grew seven points to 46, and garden/low-rise apartments increased three points to 48.

Mid/high-rise units held steady at 28, while built-for-sale units fell three points to 29. However, all four MPI components were less than the break-even point of 50 (Figure 1).

Multifamily Occupancy Index (MOI)

The MOI represents a weighted average of the three built-for-rent market categories. The study asks multifamily builders to rank the current occupancy conditions of existing rental apartments in the markets where they operate as “good,” “fair,” or “poor.”

Similar to the MPI, the index and all of its components are scaled so that a score greater than 50 indicates that more respondents report good occupancy than bad occupancy.

All three MOI components decreased year on year. The component measuring mid/high-rise apartments lost eight points to 66, garden/low-rise units declined seven points to 77, and subsidized units dropped three points to 86.

Nevertheless, all three MOI components exceeded the break-even mark of 50 (Figure 2).

The MMS was redesigned last year to offer more interpretable data while remaining consistent with the tried-and-true format of other NAHB industry sentiment surveys.

Until there is enough data to seasonally correct the series, changes in the MMS indices should only be compared year to year.

[Read more about this topic on Eyeonhousing.org]

You may also like...

-

BuilderWire

Ecommerce Solutions for Lumber & Building Materials (LBM Industry). BuilderWire, Inc. integrates the latest Internet technologies to help improve your company’s operational efficiencies and the way you sell and service customers on the web.

Schedule a Demo Today